What to Expect If Trump Wins the 2024 Election

Report Card on Inflation Control

I was interviewed last week by Yahoo Finance on immigration and its impact on inflation. They were prompted by my tweet:

If we are going to talk about the labor market, we must also talk about immigration...

I agree with @Claudia_Sahm:

"Also a very important development in 2023 -- the rise in labor force participation -- helped relieve a disruption to the supply of workers due to Covid. We solved labor shortages with more workers, not fewer customers!!! That should continue to push down inflation this year."

IMPORTANT - and this is not my political opinion just a fact that supports why labor shortages have fallen with inflation...

We have "more workers" from immigration - aka, Biden's 'failed' border policy. Stay with me...

Again, I am NOT defending this policy, but making clear that immigration is not being highlighted as contributing factor to falling inflation, because it is so polarizing.

Immigration is important to labor participation, which rolled over hard once Trump took office. Remember the obstacles in sourcing #H1-B visas? So many sent packing and borders were closed.

Well, weak immigration translates to labor shortages and elevated wage inflation - especially at the lower end of wage earners.

And the inverse is true: strong immigration contributes to higher productivity, more consumption and more tax receipts.

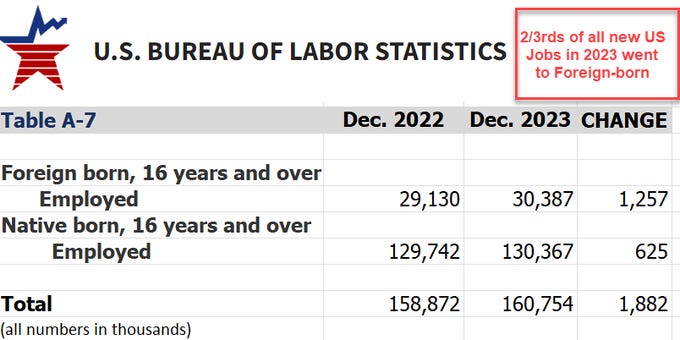

Since February 2020 - post Trump - almost all labor force growth in United States has been due to foreign-born individuals.

Some may think I am posting a political agenda. I am not. I think both candidates - Biden and Trump - are bad for America. I am also not a political pundit and hate discussing politics in my live trading room or with clients. I made a recent exception last week with our CLUB/EDGE members because I think this topic is very important to track given “policies drive inflation” and it’s an election year with potential candidates that hold diametrically opposed policies that can directly impact inflation.

Immigration

Basic premise:

Trump resisted/lowered immigration.

Biden welcomed/increased immigration.

Many can hotly debate their perceived costs/benefits, but I want to review in light of impact on inflation cost control.

Under Trump (2016 - 2020), labor participation rolled over from fewer immigrants & early retirements, as wage inflation rose on a too-tight labor market as productivity fell.

Under Biden (2020-2024), the labor force has surged in large part due to immigration: 2/3 of all jobs in 2023 went to foreign-born workers & all labor force growth since Feb 2020 has been due to foreign-born individuals. As a result: labor markets balanced, and wage inflation rose with productivity.

Some would assert that falling immigration is inflationary and rising immigration is disinflationary. Obviously, it is not so straight-forward, especially given the $9 trillion in fiscal stimulus US Govt handed out post-Covid-lockdown. But it is clear that the US would have had a much bigger inflation problem if immigrants had not been allowed to fill the demand.

Fast forward, headline inflation has dropped from 9.1% CPI in June 2022 (18 months after Biden took office), to 3.1% in Dec 2023.

Powell alluded to the successful policies in the Dec FOMC meeting:

"Not only did a recession not happen, we actually had a very strong year. That was a combination of strong demand but also real gains on the supply side."

I believe Powell’s reference to “supply side” means labor participation, which is akin to more workers to fill the job openings - and again, that is largely from White House policies around loose immigration whether we like it or not.

And because:

unemployment is low

wage inflation is sticky

productivity is rebounding

and consumer spending remains firm

so corporate profitability can grow ...

The economy has been able to with-stand global macro headwinds & sub-par real growth, as fiscal stimulus and central bank liquidity keep the equity/bond markets from cracking and causing tremors, or worse, in the real economy.

Inflation Control Report Card

I can't help but highlight these two drastically different policies on immigration - leading into and out of Covid lock-down - as a big influencer on inflation's trek. And I wonder what our economic & inflation picture will paint in 2025 and beyond should we have policies strongly anti-immigration (i.e. Trump or the like).

Until then, let's review what's working to control the cost of inflation. In a nutshell:

1. Cost of Labor & Energy:

White House has maintained loose immigration policies and tight energy price controls so as to keep inflation in check.

The former to take up much of the labor slack that can cause a wage spiral.

The latter to drive down inflation expectations.

The result is akin to fiscal stimulus that supports consumers and corporations. Motivations likely extend to it being an election year, so as to drive-up confidence in voters to support the current administration's economic policies.

2. Cost of Higher Yields:

Fed stepped down its rate hiking regime post-March 2023 bank crisis, announced a pause this Dec 2023, and is pulling forward rate cuts into 2024. This is akin to loosening financial conditions as falling yields stimulate private spending, speculation & investments.

3. Cost of Fiscal Spending:

Treasury is tasked with monetizing the growing US fiscal deficit, through Tbill & bond issuance, in addition to using USD swaps and bank facilities (BTFP, RRP, etc) that keep the largest market in the world liquid and flowing, so global markets & economies don't seize.

It is a very (so far) well-coordinated effort (with Fed, US Banks, Global Central Banks, and Congress/White House) that has supported both the equity and bond markets, and is akin to quantitative easing.

"No Landing" Achieved

All combined, the administration has orchestrated a "no-landing" by intervening - in every area they can - to control and/or influence the costs of inflation.

What to Expect If Trump Wins the 2024 Election

Bloomberg ran an article a day after I posted my report card on the current administration’s control over the cost of inflation, and how inflation could differ with Trump. Their articles highlights the differences in policies across trade, China, taxes, immigration, fiscal policy, deregulation, climate, the Fed & Energy.

Given all the potentially inflationary triggers, I am now wondering if this is the macro economic trigger that can spike yields into my 10Y year-end 2024 Prediction of 6.5%!

Immediately I got pushback:

If the markets start pounding the long end again, the Fed will wet the bed and start some sort of yield curve control.

They will pull any lever they can to try to stop the impending implosion of the everything bubble. @BurnItD0wn

I think this is pretty much 'consensus view', but let me just share why I agree THIS TIME IS DIFFERENT:

Yes, *they* will intervene again if the US 10Y spikes beyond what they deem acceptable, as they have done repeatedly before. The current leadership of White House/Fed/Treasury (with BOJ + ECB) has been active, post Trump, to a crescendo!

Now imagine… *they* aren’t the leadership anymore. Read: #2024POTUS

I know this admin sucks, but just think of the alternative:

1. Cost of LABOR rises on reversal of immigration policies (read: restricts).

2. Cost of ENERGY rises on reversal of oil policies (read: loosens).

3. Cost DEFICIT rises on tax policies (read: more cuts for corporations/less govt tax receipts).

4. Cost of INFLATION rises on trade policies (read: China tariffs/trade wars everywhere).

5. COST OF DEBT rises as treasury holders DEMAND to be compensated for “the fall of money”. Because USD will lose value and with it inflation will soar.

But what about Fed + Treasury intervention?

Fed will cut aggressively! It won’t fix the fiscal morass and corruption and fall in value of the dollar.

Treasury will continue their USD swaps to try and stabilize markets, but ECB and BOJ will be in self-preservation mode!

BOJ - our main ally globally in YCC and market intervention - could be forced to remove negative rates. The carry trade would unwind. Slowly then all at once.

More US dollar weakness won’t help. It will “look bullish” - as dollar falls and THE EVERYTHING BUBBLE GROWS EVER LARGER - but it will most certainly not be good for America’s real growth and prosperity.

"Short-term bullish, long-term bearish" is a phrase that could very much apply to our US economy should White House/Treasury/Fed lose control of inflation this election.

So as we move forward in this election year, markets will need to anticipate if the policies remain or change with new leadership, and what that will most likely mean for the future path of US inflation, economic growth and market direction.

The bogey isn't Trump, its all the baggage; Heritage Project 2025. Corporate profits are high b/c there is a safety net under workers. Remove that and two things happen, more labor pushback for higher wages, and benefits, and no public support from defunded govt agencies. On inauguration day there will be tear gas, and Trump admin will be forced to fund paramilitary operations to fight Left siding insurrectionists. There will be a depression like America has never seen. The presence of Biden keeps the Left in check, take that away and you have Civil War, and not the war you thought.

Both can change their positions after the elections. And I hope in a more pragmatic direction. Both have done that.