What If Yields Crash Down Not Up?

CLUB/EDGE client post May 7th. Focus on my "BONDS ARE BACK" call April 30th.

» CLUB/EDGE client post Tuesday May 7th 5:59 PM

First The Micro: SPX 5200 HIT - from April 20th.

As I warned this morning: A tussle now at $5200 and QQQ 442 makes some sense as 10Y yield bounces off its 10W at 4.42%, but we still have higher Nasdaq to tag still, which likely brings the 10Y down to ~ 4.33%. And VIX down to 12.70 before a higher probability reversal. In both.

Maybe we fade into CPI next week then reverse higher. I'll watch SVXY + BXM for tells with volume and breadth, but right now, none of these are weak.

That means, it is more likely the "Call Wall" for dealers adjusting their stocks. Above and call chasing could get busy.

So, for now: Below 5200 intonates lower gaps can fill on the hourly: 5131 + 5068

Once we get/stay above 5200, this will likely mean my $5340 2024 SPX is back on the table.

I say likely because I really NEED to see how the 10Y handles 4.33 with overshoot to 4.2%.

EMPHASIS: I NEED TO SEE THE 10Y YIELD GET/STAY BELOW 4.2% TO REALY EMBRACE A BOND RALLY.

So What If Yields Crash Down Not Up?

If 10Y gets/stays below 4.2%, I will admit: Everything changes. Here's my initial thinking on what that *could* mean.

Fed Pause and Yellen Yahtzee on November 1st with the 10Y yield at 5% and much higher term premium was INTERVENTION. But each round of intervention has had a diminishing rate of return on both the economy and markets, so I am now focused on how far the recent intervention from last week (mild by comparison) will last for equities.

I am then watching the level at which falling 10Y can fall and NOT be bullish equities. I think 4.3/4.2 is fine, but below that and we have an economic warning that is equity bearish.

The 10Y has been chopping wildly around an ascending 200D as both move higher. Breaking and staying below the 200D is no bueno. We can have a move closer to deflation than dis-inflation. This is not my baseline-bet, yet, but I must keep an open mind.

I am not in the camp they will hike or cut in an election year, but the bond market is pricing in a soft landing giving them a free pass if they do cut. The 2/10 curve I show clients daily is actually starting to break down, which is a bull flattener not steepener. This implies the HFL nominal rates (hikes = inflation + higher assets) is starting to lose its structure. I can see a case where the falling 2Y10Y yield curve finally breaks down to -.60% which will pull forward the #HFLUR (higher for longer until recession) call I made end of April.

Big Tech is spending on CAPEX, higher costs of capital, and itself (stock buybacks). Their moats will narrow. Falling yields will not be as bullish tech as many think. I see money to continue to rotate into XLU, XLP, XLV as catch up trades. Think: non-cyclicals.

My "Warm Summer Housing Market" call will likely support mortgage financing and insurance companies, as homebuilders stay bid even as the economy weakens. "Buy the rumor, Sell the news" into recession kinda play. But the "mobility trade" as I like to call it won't really move the needle for oil or equities in general. It just helps housing tightness find short-term relief and pent-up consumer demand drain savings and take on more debt.

Bonds will rally on falling yields but regional banks still don't look safe. Also Fed will be slow to cut while other countries do. Good for fixed income that invests in bonds abroad.

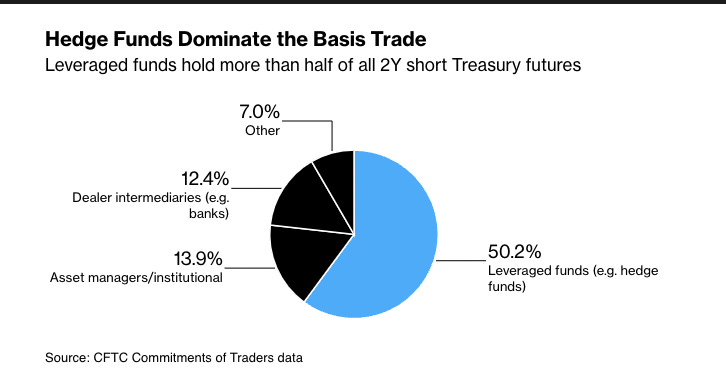

The "Basis Trade" is at risk of reversing, for real, if yields fall below 4.2% 10Y and stay below.

Credit spreads should widen then as well, which would really not be good for tech/equities, as future earnings (multiple expansion hopes) are revised lower.

Fed cuts will be pulled forward but not for bullish equity reasons, but because banks and labor and economic growth will slow. Inflation won't be the focal point. Disinflation will be. Falling tech, semis and bitcoin will be blamed on 'fading AI hype' or the like, but it will really be a CONTINUED rotation into non-cyclicals as safety - with bonds, gold and dollar.

But I NEED to see the 10Y yield break not just 4.3% but get/stay below 4.2% before I can truly embrace the breakdown of the Basis Trade + the like.

Otherwise, at some point later this year, I still see the 10Y yield getting and staying above 4.688 that will put in play my 5.3%, potentially 6.5% 10Y yield call into EOY/Q1 2025.