USD Has Likely Peaked - Revisited

Update to my November 2023 market timing call.

Bank of Japan "surprised" last week in its March meeting with a rate "hike". I say surprised, but Nikkei Asia had been leaking it for months. I say hike but in reality they just ended their negative yield curve control policy to raise its benchmark rate to 0%. It was not a major change, and market didn’t seem to react negatively, despite USDJPY pushing back into a level of prior MoF/BOJ intervention: 152.

So, now, how will they potentially cap the JPY or JGB yields from making big moves? Well, the BOJ will continue to purchase their bonds, of course! But they did say they will stop buying their market’s equities, for which they currently own the majority of around 60%, which, by the way, they could turn around for a profit given the outsized Nikkei performance over the past year which has breached 1989 highs.

The yen is currently very weak, and that begs the question:

Will they let the yen fall further?

If they do, will it create a currency crisis?

If they don’t, will they raise rates more quickly to stem the risk?

That brings me to the yen carry trade trigger unwind risk, and my big call for CLUB/EDGE clients last November that the "USD Has Likely Peaked".

First, let’s review my call, highlight why gold plays a critical role, how the USD weakness threatens any bond bounce, and then circle back to the risk of a yen carry trade unwind that would threaten the equity advance - especially from a surprise US Presidential election outcome.

Review of My Call : "USD Has Likely Peaked"

It was November 9th when I made this call and presented it in an interview with Roger Hirst of Lykeion:

USD would fall

Equity markets would be well supported because of it

The 10Y yield would fall from 5% to 4% then be range-bound for 2 quarters - between 3.8% and 4.7%

(Before moving above 5% and into potentially 6.5% end of year.) Yeah, that is still part of this market timing call...

A lot of that market-timing call was based on my read of the 10Y yield rate of change and what I expected would be the motivations of the powers-that-be to keep markets supported at the time oil, dollar and yields in check into the election.

March 1st of this year I reminded clients I still didn’t see a directional move with bonds of size for more than a trade:

"MUCH chopping in a channel versus a directional move out of its channel: 3.8% to 4.4% gives it a lot of room to head-fake yen, bond and gold traders.

UNLESS the USDJPY gets/stays above 152, or some other macro risk enters, to trigger a potential carry trade unwind, which could be very disruptive to the short Treasury/long Nasdaq bets that would also need to unwind.

More likely, US yields + DXY will be range-bound in an election year versus spike higher triggering a duration shock for equities.

I firmly believe, without an exogenous event, these assets are in the "not allowed to go up TOO FAST category" with oil.

Also in this category is Gold."

Gold’s Critical Role

Gold moving too high would be very problematic for central banks. Some might say the recent break out above all time highs in gold foretells a well-disguised macro risk of war, currency wars, and/or debt debasement. Others know the debt load of the U.S. is growing at ~ $1 trillion every 100 days making hard assets like gold a store of value over the dollar or US treasuries, even if it earns no interest.

Our MacroAdvisor EDGE Manager, Craig Shapiro, sums up the value of gold relative to the current slow trend of de-dollarization:

"The USD can rally against other fiat currencies, because we still have the highest yields and the best growth trajectory with a Fed that will be slower to add accommodation than other central banks.... but down against hard assets like gold.

Gold is a structural long... as the world becomes more multi-polar and gold increasingly enters the fray as neutral reserve settlement asset for excess trade surpluses.

On any given day it can be driven by USD strength or weakness or real rate moves, but the structural trends are that the East is buying more gold every day and the price is moving higher as gold can buy more energy and other commodities over time as they trade away from the USD."

The world is slowly embracing structurally higher interest rates - especially Japan given its debt to GDP of ~250% - at the same time both Japan and China weaken their respective currencies against each other to maintain a lead in global export markets, and as both have been transitioning to buy energy outside the USD.

Gold is a hard asset and reserve currency that will gain favor, especially as the dollar weakens - less to other currencies, but more against hard assets.

USD Weakness Threatens Bond Bounce

At the end of this post you will see exactly what I wrote for clients Nov 10th.

But I want to highlight two core themes I don’t want lost or ignored.

The Bullish Bet:

"the bull case for emerging market, equities and gold with select commodities is when Fed starts cutting rates against a backdrop of declining dollar."

This has already been playing out - from higher prices in food/agricultural commodities to precious metals to industrial metals. (Oil is not in this camp as I see it as an "embargo trade", not allowed to go up into the US election.)

And why I said a falling dollar was "so bullish it's bearish" equities. Short-term gains for longer-term pain.

The market is asking UST holders to compensate for “the fall of money”, but market doesn’t see it yet.

Fast forward, equities have 'mooned', but gold has too.

Given gold's advance, gold is warning that this inflation problem is a fiscal problem.

As Geoffrey, our MacroAdvisor EDGE Contributor, has lamented often:

You stop avoiding the elephant in the room. Trying to look for the elephant under the carpet (QT), behind the cupboard (QE), under the sofa (QRA), while it's right in front of you. You rescind this stupid "unlimited spending": put your budget & trade in order. NO OTHER SOLUTIONS

He’s spot on, and why I also framed last November that longer-duration bonds held "unattractive risk/reward" for more than a trade.

USD Weakness Threatens Bond Bounce

Falling DXY and softer yields may have served as a strong tailwind for equities, but I see it more as a headwind to a durable bond bounce.

And here's why: As rates fall (especially with Fed rate cut bets surging), demand for USD and UST will fall together and this will be negative for risk assets.

This is not your credit event/crisis that forces USD crowded longs. We have a whole new regime of quasi-fiscal deficits under the mechanism of Fiscal Dominance now.

Since market can’t price THAT in, given all the tricks Yellen is pulling out and Fed is forced to defend, foreign money is going back home/abroad.

By the way, this is another big tailwind for gold.

Yen Carry Trade Unwind As Threat to Equity Advance

November 16th, 2023, I wrote that the market looked very "1999-esque", then "doubled down" bullish mid January, posting a SPX price target of $5340 for 2024. I’ve been interviewed by MarketWatch and Bloomberg with my "Everything Rally" thesis.

We are very close to this mark, thanks to not only weakness in the USD, but also abundant liquidity from loose monetary policies, Treasury bill issuance instead of notes/bonds, fiscal spending (and debt forgiveness), promises of Fed cuts, falling inflation expectations, even more fiscal spending, and of course, FOMO & tech concentration risk over AI potential.

As a result, options market has stayed firmly long and strong in a seemingly infinity loop of positive gamma.

What would interrupt the flows and have dealers flip and press gamma short?

February 18th I wrote my top-of-mind Macro Triggers that could really matter, eventually:

PBOC yuan devaluation (tough to time; would be a surprise)

BOJ rate hike/normalization (USDJPY above 152 could intonate)

Term Premia spike on longer-duration bonds (confiscating Russian assets would do it)

Oil spike (and one that sticks)

Debt Issuance of more bonds than bills (April 30th is next QRA)

POTUS election year surprise (#RFK odds are growing)

Government Shutdown surprise (March 1st next dance)

Unknown Black, Grey, White Swan (definition of unknown unknown)

So now that the BOJ has removed negative rates from its policy... Does the Carry Trade Unwind Threaten?

I have said before, that the USDJPY is akin to rudders in an attack submarine.

DXY is the engine.

JPY is the ballast.

10Y the diving planes.

And the Pressurized Hull of this stealth sub is what keeps everything inside it under water from being crushed.

This is why I watch USDJPY + USDCNH rising as a tell for risk off in equities!

Food for thought from my November client post:

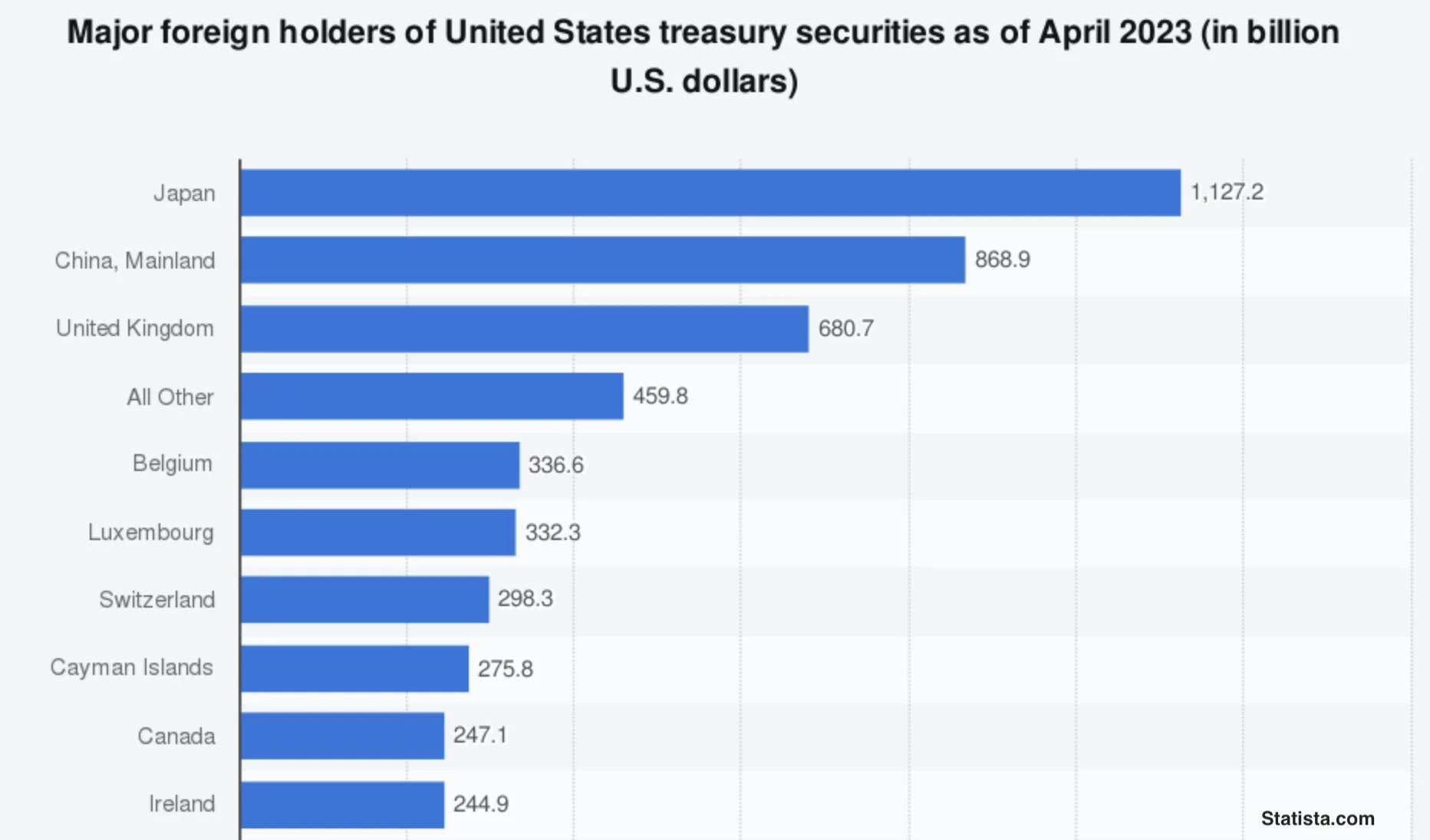

Japan is the largest holder of US debt and equities, holding over 1.1 Trillion US dollars worth.

BOJ is making hawkish sounds just as the rest of the world's central banks are pausing/cutting.

2021-2023 were the years when the Yen had an incredible bear market due to YCC – which happened to take place during the fastest Fed hiking cycle in history.

So what happens to US bonds AND equities if the opposite occurs in 2024-2026?

If/When BOJ reverses negative rates and pivots, there could be an exit from the dollar to the yen.

This was the basis of my client post last year, and now that we are here, it bears careful watching.

The Rise Of Carry From US Presidential Election

Big Picture: The Rise Of Carry - And It's Unwind - is likely very slow and well-orchestrated.

But I wrote about the potential of a "carry trade unwind" picking up speed depending, in large part on the future policies from a new POTUS. For example: What to Expect If Trump Wins the 2024 Election

We know what to expect from Biden - more of the same. But from RFK Jr? We do not know what to expect, and this is not 2016 when Trump was last President.

My point is simply that we have risk dead-ahead, and given my above analog that DXY is the engine, JPY is the ballast, and 10Y the diving planes, it will matter greatly what policies are adopted should a new President be elected.

For a great listen on the carry trade in general, here is an excellent podcast featuring Kevin Coldiron on a book by the same title: Rise Of Carry.

He has a great point I want to summarize/ highlight:

The “Fed Put” works to add liquidity in a DEFLATIONARY world when bonds are bullish.

But I contend that:

In a world of entrenched inflation and endless money printing, the most deflationary assets are... the USD and US Treasuries.

I also firmly believe we have transitioned from a monetary dominance to a fiscal dominance regime.

Policies that ignore to address this risk, force the transition from the the carry-trade to the anti-carry trade - a world where the Fed put (monetary easing) & Yellen "Yahtzee" (my expression for endless bill/bond issuance to fund fiscal largesse) trigger inflation.

And nothing short of controlling Fiscal Spending will help get control of inflation.

Basically, my THINGS OVER PAPER mantra since July 2020, and why INFLATIONARY REAL ASSETS should outperform during this transition.

November 10th, 2023 Client Post

USD Has Likely Peaked

This may be early, as I didn't expect to be writing about this until next year as recession fears grow louder, but I think it bears discussing after a very large drop in DXY last week that broke my $105.77 weekly 'must-close-above level.

Geoffrey is already all over how our currency is at risk.

“If the yield curve continues to flatten or even steepens, it can indicate that the central bank is losing control over anchored inflation expectations.”

We can see that in this morning's UMich report to which Craig weighed in promptly:

Extremely firm UMich inflation expectations with 1 year rising to 4.4% and 5-10 year up to 3.2%, which is a new cycle high.

We continue to throw caution onto the idea that inflation expectations are well-anchored. With softer growth readings, we are moving into the stagflationary camp at an accelerating pace.

Expectations for rate cuts to address the growth concern are misreading the Fed's reaction function. We need to see way more risk off first to get the Fed anywhere close to providing stimulus.

Geoffrey reminds firmly: The inflation problem is a fiscal problem.

You stop avoiding the elephant in the room. Trying to look for the elephant under the carpet (QT), behind the cupboard (QE), under the sofa (QRA), while it's right in front of you. You rescind this stupid "unlimited spending": put your budget & trade in order. NO OTHER SOLUTIONS

So what does this have to do with my focus on dollar peaking?

Because we have crossed the Rubicon where Treasury will print and print and print, not deterred by higher rates.

“For irresponsible governments, debt is not debt its just money.” Geoffrey #graphcall-macro-education

With that, it is growing more obvious that foreigners are reluctant to finance America's fiscal deficits.

US Treasury reports:

Foreign official holdings of US Treasuries have declined by 12% from US$4.25tn in July 2021 to US$3.76tn in July 2023, the latest data available, though up from a recent low of US$3.61tn in October 2022.

China’s holdings of US Treasuries have declined by 26% from US$1.1tn in February 2021 to US$822bn in July, while Japan’s holdings are down 16% from US$1.33tn in November 2021 to US$1.11tn in July.

This is also the related reason for the decline in the US dollar's share of foreign exchange reserves (see chart below).

USD Weakness Threatens Bond Bounce

Falling DXY and softer yields may have served as a strong tailwind for equities, but I see it more as a headwind to a durable bond bounce.

And here's why: As rates fall (especially with Fed rate cut bets surging), demand for USD and UST will fall together and this will be negative for risk assets.

This is not your credit event/crisis that forces USD crowded longs. We have a whole new regime of quasi-fiscal deficits under the mechanism of Fiscal Dominance now.

Since market can’t price THAT in, given all the tricks Yellen is pulling out and Fed is forced to defend, foreign money is going back home/abroad.

All this debate around soft or hard landing, focused on strength of consumer spending and corporations maintaining tight margin control on declining revenues, misses the point!

Wage inflation and US govt spending as stimulus will tip the growth mantra into recession as corporate revenues AND margins slow from falling demand of USD and US Treasuries.

Repeat: The market is asking UST holders to compensate for “the fall of money”, but market doesn’t see it yet.

Currently, many feel equity valuations are too high to chase here and long-duration bonds aren’t cheap enough to buy safely. So we grind sideways in big swaths - not breaking higher, not breaking lower.

And that is going to help Yellen keep equities correcting in time more than price until the next exogenous event triggers or a Treasury QRA or bond auction disappoints.

Until then, the bull case for emerging market, equities and gold with select commodities is when Fed starts cutting rates against a backdrop of declining dollar.

Bank Of Japan Pivot Is Bearish US Dollar

The Bank of Japan’s Kazuo Ueda is in a tight spot. If he stands pat on policy he risks sending the yen to a multidecade low and opening up his yield control program to speculative attack in the market.

At the same time, if he raises the ceiling on 10-year yields under yield curve control — explicitly or implicitly — the governor may invite long-term rates to rise to levels inconsistent with economic fundamentals, jeopardizing his goal of achieving stable inflation - not to mention his job.

Adding to the difficult decision, each round of bond-buying offers up diminishing returns, calling into question the viability of the bank’s easing program altogether.

Brad Setzer makes a compelling case in: The Disappearing Japanese Bid for Global Bonds

The rise in Japanese holdings of foreign bonds had an enormous impact on global markets between 2011 and 2020. The markets will now have to adapt to a sustained reduction in Japanese demand.

So why would Ueda at BOJ announce an end to the negative rate policy?

Here's a detailed version why: The Bank of Japan Experiment

And why it will matter when they do:

BOJ is allowing the USTs they hold to mature off their books or outright selling them and using the USDs to buy and stabilize the yen.

Given Japan is the largest holder of US Treasuries, holding over 1.1 Trillion US dollars worth of debt, it matters when they sell as it puts upward pressure on our longer-duration yields!

And until the BOJ fully relents and allows JGBs to trade at truly market driven prices, this will only get worse, adding significantly to the pressure on the US 10yr UST.

2021-2023 were the years when the Yen had an incredible bear market due to YCC – which happened to take place during the fastest Fed hiking cycle in history.

So what happens to US bonds and equities if the opposite occurs in 2024-2026?

Chances of a BOJ pivot are rising: https://www.japantimes.co.jp/business/2023/11/09/economy/boj-policy-meeting-opinions/

If/When BOJ reverses negative rates and pivots, there could be an exit from the dollar to the yen.

The mechanics are complex but roughly translated:

Japan's large foreign holdings of US debt is widely regarded as the spread trade.

The price of the yen is directly related to the difference in yields between US and Japan's 10Y bonds.

The spread trade involves Japanese investors selling their Yen in favor of USD to take advantage of the rate spread. US bonds currently offer far higher rates than Japan.

If the spread trade were to unwind, Japanese holders of US debt would sell their US debt and move back to the Yen, creating a likely disruptive outflow from US debt and equities.

If the spread trade collapsed, Japanese holders would be selling their USD in favor of Yen, creating a likely disruptive outflow that would trigger cross-asset currency volatility.

A BOJ pivot on rising inflation, would cause the spread between US and Japanese yields to tighten, creating lower demand by Japanese investors for US bonds and US dollars .

A continuous increase in the Japanese Yen, or Japanese yields, could induce further spread trader selling, putting more upward pressure on US longer-end yields and downward pressure on US dollar.

Which brings me back to my opening argument: USD Has Likely Peaked.