Trouble In Paradise

CLUB/EDGE client post Tuesday, September 10th, 2024. Focus on narrative flip to recession risk pulled forward; bullish macro trigger needed pronto; and US 2Y yield as "tell" ala 2008.

» CLUB/EDGE client post SEPTEMBER 10th, 5:03 PM ET - as KEY levels for 10Y yields, crude oil & USDJPY needed to get defended to be bullish for “One More High”. We got the 50bp rate cut Sept 18th - which serves as the “bullish macro trigger needed pronto”.

It's a puzzle I like solving. And betting on highest-probability motivations ;-). I've said repeatedly: *THEY* can't let yields & oil & usdjpy fall too much. AND most definitely not before the election. ;-) Then it's a matter of finding those levels or pressure points where they MUST do a POLICY INTERVENTION. And. THEY. Did.

Time To Flip The Script

That was fast...

I've been talking about a narrative change coming ;-)

Reasons why investors need to prepare for a US recession.

The Fed is unlikely to save the day as economic conditions deteriorate.

Investors were right to favour stocks over bonds for the past two years. Now, it is time to flip the script.

Financial Times

This weekend brought several such articles and macro posts out of hibernation - some free and some for fee, but all warning Winter is Coming and with it a cold-spell that could turn into frigid conditions for equities.

Now watch the narrative shift from even the most ardent bulls to:

"The US economy is cooling in response to tight monetary policy, as evidenced by falling inflation and wage growth."

"A softening labour market will undermine consumer spending. The personal savings rate stood at 2.9 per cent in July, less than half of what it was in 2019."

"Consumer loan delinquency rates have risen to levels last seen in 2010, a year in which the unemployment rate was double what it is today."

"If housing construction continues to weaken, we will see a wave of lay-offs in that sector."

"Default rates are climbing in the office, apartment, retail and hotel segments. Regional banks, which account for the bulk of CRE lending, will experience more losses."

"Core capital goods orders have been trending lower for the past two years. [Construction] spending has peaked and will decrease over the coming quarters."

"The Federal Reserve is unlikely to save the day. The economy succumbed to recession just months after the central bank started lowering rates in January 2001 and September 2007."

First it was a negative MoM CPI print to put the fear of deflation into the hearts of market bulls, who later mocked the bears after the sharpest VIX reversion in history August 5th, only to worry again after negative job growth forces them to ponder if there might be trouble in paradise.

Doesn't Look Good

I have been very consistent in my well-timed warnings and levels.

10Y YIELD - well below my 3.8% line-in-sand. In fact, it tagged QTRLY support Aug 5th at 3.678 and has broken below even that!

BANKS - finally succumbing to the pressure that I warned about for WEEKS: falling yields hurt net interest income!

OIL - my view from April that crude would fall to $70 then once below on weekly support would fall to 65.65 monthly support then once below that it would really pick up speed; in time down to $40. We are at 65.65!

USDJPY - my target of 142 - literally JAN 2021 trendline tag - is here after warning clients July 13th to prepare!

CONCENTRATION RISK - The last time a MAG 7 stock made a new ATH on a CLOSING basis was over 60 days ago on July 9th. This is THE DAY I warned for a growth-to-value rotation of size (RSP:SPY chart below 2003 lows). It's still in play!

CARRY TRADE UNWIND - is all about higher yen, lower yields, lower oil.

Translation: Shorting yen & bonds while long oil & NDX is the CROWDED TRADE. That's what we see.

This is what we can't see: How much leverage and how much counter-party risk there is at every level of the carry trade.

All of the above makes me super aware how badly we need a MACRO trigger that is bullish, because the lack of it will trigger more LIQUIDITY DEFLATION which forces LEVERAGED counter-party risk to cover long their short yen, short bond trades and sell their long oil, long NDX positions.

This is the perfect storm for more forced deleveraging.

Bullish Macro Trigger Needed Pronto

So as I survey the landscape of potential bullish impulses to get the 10Y back above 3.8% and Crude oil back above $70, to help suppress yen, bonds and volatility, so we can have a nice swing long in growth/tech plays - even if just a rotation - I am having a really hard time finding a MACRO trigger that is bullish.

Trump - Harris debate? They will both spend. They are both inflationary. Is that enough?

CPI/PPI? Both are trending lower and expected to trend even lower as oil, rents and inflation expectations fall this quarter.

Fed cutting 25 bp? That's not gonna move the needle given Fed Funds Rate is pricing in 200bp of aggressive rate cuts in the next year.

I keep reviewing my recent clients posts/themes:

Growth Story for MAG7 reached "As Good As It Gets" Q2

Powell eviscerated #HigherForLonger at Jackson Hole

Recession Risk Is Pulled Forward from falling yields & oil. Awaiting higher unemployment shoe to drop next.

Buyers are Stepping Away from Equities and rotating into non-cyclicals, defensives, safety.

Liquidity Deflation of Assets and Bond Rally means Long Defensives (XLV, XLP, XLU, XLRE, IHI) and Paid To Wait

July 26th bears repeating:

"One More High" is a probability, but with Global Central Banks now cutting rates as demand for credit falls, we are on the cusp of pulling forward recession risk from 2025.

And with the US 10 year yield 150 basis points below the Fed Funds Rate, Fed is behind the curve.

I continue to expect the narrative to switch from inflation to deflation into year-end."

Yield Curve DIS-Inverts. Now What?

Investors are jittery for another reason.

When the 10Y2Y yield curve inverts, it suggests recession is coming! But this measure has been inverted for two years and no recession!

As I have suggested, Inflation (and especially Wage Inflation) delayed recession.

Fast forward, inflation and economic growth have slowed.

Dis-inversion now suggests a recession is imminent as Fed rate cuts in the next two years will be enough to ensure that shorter rates are lower than long ones.

I can see another case where the Fed cuts aggressively forcing the 10Y2Y back into inversion.

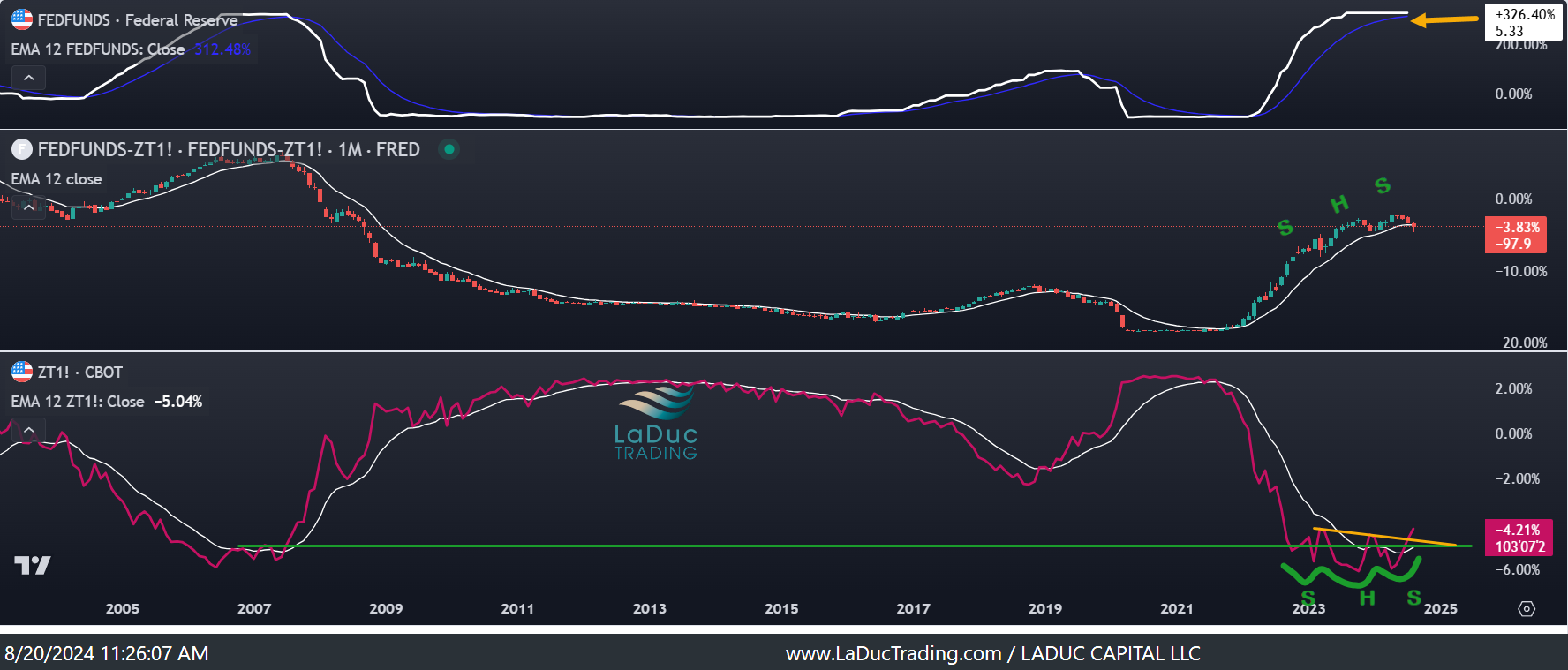

For now, the two-year Treasury yield has been my tell as I warned: we are Topping Into Year-End - [Detail update in member’s slack workspace August 23, 2024].

The curve between 2Y yield and fed funds rate, which I have shown repeatedly of late to predict falling yields, is actually at its most deeply inverted since the beginning of the crisis year of 2008!

Back then, traders accurately thought that the deepening credit crisis would force the Fed into cutting many times.

That’s the history we keep.

But 2008 never had the carry trades and amount of leverage in our current equity market.

There is a lot more to unwind.

Brilliant! I'd add $SOXX may be confirming a bearish 10/30 week cross with a H&S pattern. Leaders lead.