Stagflation With A Side Of MONEY GOES HOME

Summer Recession

Monday morning I discussed how Asian Currency Risks Grow.

This morning in my live trading room I reviewed the Trade Reset Scenario Timeline (courtesy TradeTheNews) on recent reports by Citibank & Apollo Analysts pointing to a summer recession on supply chain disruptions to economic activity.

Here are the notes:

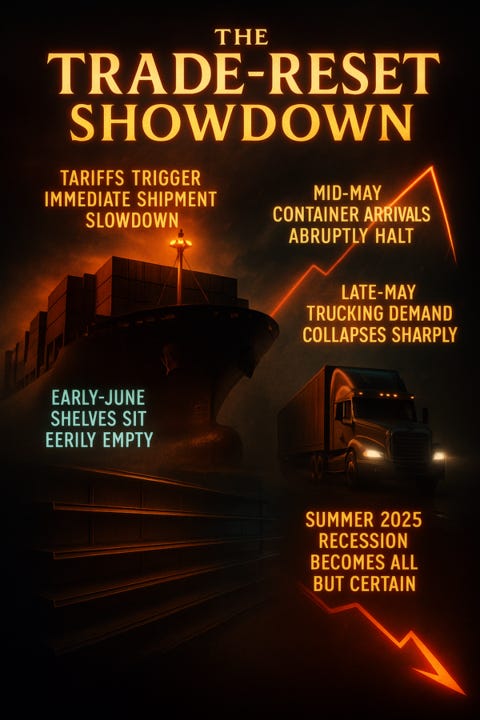

Early to Mid-May: The Shipping Standstill (Citi & Apollo)

20–40-day transit lag: Containers that sailed before April 2 arrive at U.S. ports in early/mid May—then have nowhere to go.

Port layoffs: Idle berths at Long Beach, Savannah and beyond trigger furloughs among terminal operators and longshore workers.

Tariff revenue: Citi forecasts a brief peak in customs receipts from China before revenues decline, reflecting the rising influence of non-Chinese exporters.Mid to Late-May: Freight Freeze (Citi & Apollo)

1–10-day rail/truck window: With fewer imports, inland carriers face a collapse in loads.

Driver layoffs: Trucking demand falls off a cliff; Citi’s logistics team and Apollo both note widespread layoffs.

Diesel demand: Citi’s energy analysts estimate diesel consumption in freight to drop 30–35?percent, squeezing fuel suppliers and energy equities.Late-May/Early-June: Retail Reckoning (Citi & Apollo)

Empty shelves: Warehouse stock turns slow dramatically as Southeast Asian substitutes fail to fill the Chinese gap.

Retail layoffs: Declining sales prompt staff cuts at big-box and specialty retailers alike.

Inflation lag: Both Citi and Apollo warn that price spikes born of genuine scarcity only register in official CPI and retail-sales figures in June/July.July 8: The Wild Card (Citi & Apollo)

Pause expiry: Citi strategists caution that a failure to extend the 90-day moratorium will reignite cancellations and layoffs.

Apollo’s scenario: No vessel will book past July 8 without clear policy guidance—setting up a second half-May style convulsion if the pause lapses.Summer 2025: Into the Maelstrom (Joint Take)

Citi and Apollo analysts converge on four lessons for the U.S. economy in mid-2025:

Built-in lags—Policy shocks rip through shipping, freight and retail over roughly three months.

Elastic trade patterns—Short-term winners (Vietnam, Thailand) gain pricing power, but cannot match China’s scale overnight.

Synchronous risks—Energy, transport, retail and consumer spending all buckle around late summer 2025.

Policy constraints—With the Fed set against inflation and Congress gridlocked, monetary or fiscal backstops will be limited.

Stagflation With A Side Of MONEY GOES HOME

Given the backdrop of tariff-induced supply logistics nightmare & threatened layoff tsunami, I have reminded that prices paid (above 60%) is a growing concern amidst economic contraction.

Unlike during Covid when demand was high, these supply-induced high input costs are coming when the consumer and companies will not be buffered with stimulus.

Higher prices will not be easy to pass on to consumers, so company margins and revenues are expected to suffer. The market isn’t pricing this in but instead expects trade deals to materialize before economy triggers real not just perceived recession.

While we wait for hard data - starting with rising jobless claims, Fed will push back on rate cuts as capital hill debates tax cuts. Fed Day will be as expected with June normative cuts getting slowly priced out.

The prospects of completing a debt ceiling deal by Memorial Day grow dim, pushing the risk of no-deal to June.

In the meantime, Bessent floats a headline tonight that he is flying to Switzerland to meet with China trade representatives. Of course, this news is met with a market bid... but market has been disappointed often by hopeful headlines. I am still waiting for VIX 20 pattern to emerge before I can get too excited either way.

In the meantime, gold is not waiting. It smells all of the above and isn't waiting on a trade deal or fed cut or tax cut or debt ceiling deal. It is just doing what gold does in a backdrop of rising inflation and falling confidence. IF Bessent is successful, expect a strong rotation out of gold and into equities. I said: IF.

Bonds too are reacting to all of the above recession risk and trade policy uncertainty.

The bear steepener in the 10Y2Y yield curve is also performing its function to signal higher 10Y yields from -

bondholders demanding more for the duration and fiscal risk

foreign investors selling and repatriating money back home

fund rebalancing out of bonds and into stocks in hopes of peace deals, trade deals, tax deals...

As I wrote about back in December, a better place to buy bonds is after we have steepened into +90bp.

So far this has been working well, as has my call for crude oil to roll over this year.

The Permian going bankrupt isn’t on many folks’ BINGO cards!

But Geoffrey provides the fundamental reasons to our clients for doing so! Check out his channel: graphcall-macro-education

Falling global oil demand was predestined even before falling global credit demand & falling global economic contraction from trade wars.

It was last April I called for Crude oil to fall into $60-40 range this yr & stay there awhile. As of June 2024 when WTIC was $80, no one believed I saw it getting cut in half. Now they do.