Quarter Ends & Gold Hits New Record High

CLUB/EDGE post with focus on precious metals.

Global Markets in Q1 of 2024 outperformed. It would be UNUSUAL to expect annualized results.

Consider, for example, SPX returns of 10% past 3 months equating to 40% return by year end. Or the 20% return in Nikkei equating to 80% by end of Q4 2024.

It's just not very realistic.

Especially as the AI mania has quieted past month or two, exactly at the same time Fed rate cut expectations have dimmed.

Case in point: Today we got the first US ISM Manufacturing PM over 50 in 18 months. That put a bid in yields. ISM Prices Paid reading of 55.8 (vs. 53 expected and 52.5 last month) caused June rate cut expectations to fall to 56%.

We know: above 50 is expansion and below 50 is contraction. And it's pretty safe to assume: Expansionary Manufacturing is Inflationary.

Craig, our MacroAdvisor EDGE Manager, takes it further and posted for clients earlier:

It looks like we could have a replay of the October 2023 trading period where we get $ up, yields up, oil up, however this time, the economic momentum remains firm with labor market "very very strong" according to Powell and inflation having already started to re-accelerate.

So the setup into this month's IMF meetings and May 1st Fed meeting and QRA announcement is a bit different as the economy seems a fair bit better now than what they were worried about last fall which caused the Yellen/Powell pivot on November 1st.

Back then, the Fed was able to see the deceleration of inflation and tell the market that no more hikes were needed. The long end was doing the work for them, financial conditions were tightening and the economy was reacting.

This time around, they want to start the cutting cycle but the data continues to positively surprise and there is a growing contingent on the Fed (including a hawkish voting block of Bowman/Bostic/Waller/Barkin) that don't seem ready to start. Financial conditions are incredibly loose and it is really not clear that current monetary policy is restrictive at all.

We should be trading a growing probability that the Fed will not be able to cut rates at all this year. If the labor data this week confirms this "very very strong labor market" (Powell's words, not mine), we are going to lower the odds of a June cut and then we should also be lowering the odds of cuts starting later this year as we get closer to the election. July meeting falling during the conventions add an extra degree of difficulty to cutting then (unless major data deterioration) and September is just too close to election to start a cutting regime.

I have been saying that risk assets would top when the odds of the Fed's next move being a cut were equivalent to the next move being a hike. We seem to be moving further down that line now. Let's see how risk assets handle the transition.

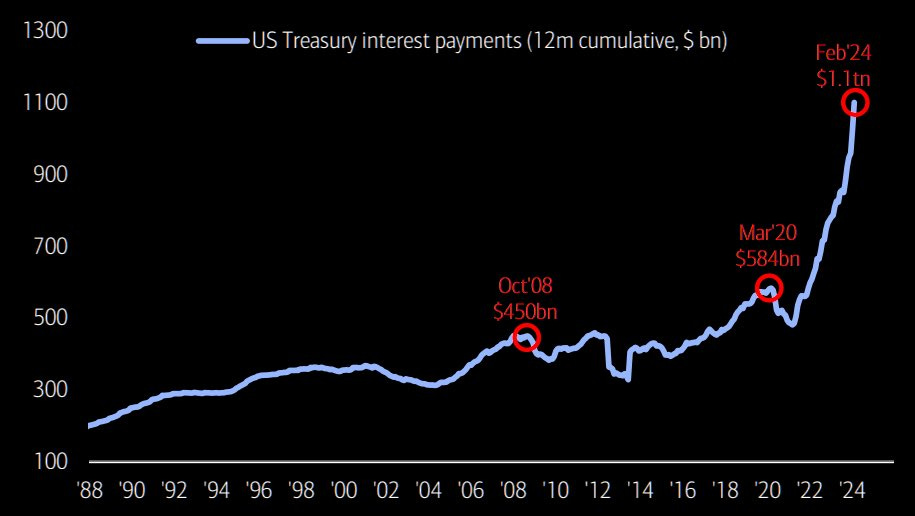

Chorus of "US Government Debt Is Unacceptable" Grows Louder

Citadel's Ken Griffin is out with an investor letter for the first time in years:

The current US administration is being irresponsible in spending ; a record 6.4% non-recession deficit is too high when unemployment is only 3.75%. Our debt situation is not sustainable.

Bank of America's Hartnett is estimating:

US government spending past 5 months = $2.7tn, up 9% YoY…on course for $6.7tn in FY24; US national debt rising $1tn every 100 days…set to hit $35tn in May'24, $37tn by US election, $40tn in H2'25

This is the reason for the season in spiking higher interest rate costs on that US government debt.

For this reason and many others, gold has caught a bid since my March 1st warning:

Tail Wagging The Dog; CRASH UP on hold until after March; & Gold as a Tell

Still Bullish Precious Metals

Gold hits new record high of $2,259 an ounce today on Easter Monday when London/Europe is closed. Congrats to longs, and those who held post FOMC ;-)

Here’s a client who couldn’t take the sleepless nights from WINNING so much on this trade:

I have been relentlessly focused on this trade for clients since we had a solid breakout in Gold, March 1st. It continues to dance higher, but there will be music changes.

Right now the strong USD and weak bonds may be intonating that those who NEED to pay for rising commodities in USD are selling US Treasuries to do it. Dunno for sure, but it will be very telling should USD weaken and commodities stay bid, which is what I expect.

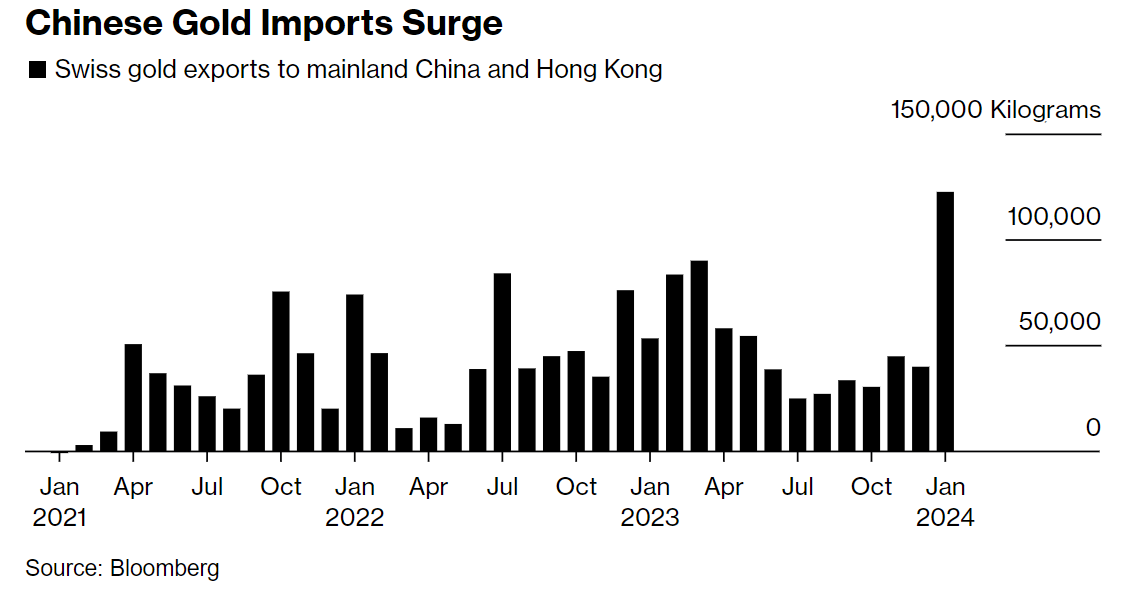

Here is a highlight of last week's Macro EDGE Roundup where Craig discusses the multi-faceted work at play with gold serving as neutral reserve asset.

Also, a chart of Chinese Gold Imports, which are surging in China and Hong Kong, not to mention India etc.

Chart courtesy @JasonEBurack, whom I will interview soon on the mining space, thinks:

Q1 2024 earnings we should start to get some top and bottom line beats from gold royalty companies and gold miners.

Many gold stocks are going to be re-rated by bank analysts in the coming quarters if metals prices stay at these levels or go higher.

Cash flow projections will be raised. Share price targets, too. And hopefully, top and bottom line beats of analyst estimates...

Point was made well in advance by Geoffrey a few weeks ago:

The UST market will implode. Commos ramping from soft to Precious to indus and Fed dis-anchoring? It's a pressure cooker on USTs.

The release valve is GOLD, SILVER & GOLD/SIVER MINERS.

Will "Sell In May & Go Away" Time With NVDA Earnings?

With WTI crude above $83; USD moving higher with gold; inflation staying sticky/strong... I would suspect that Fed cut expectations getting pushed out can cause this "Everything Rally" to get tested. Especially tech. Especially if we get a growth slowdown as shown in tech earnings this month.

Speaking of which, NVDA has earnings May 22nd. Consider what happens to the market if they disappoint? Do you think LIFO longs will wait until then before lightening up?

I contend, NVDA is already in distribution mode past month plus. That and my intermarket analysis clearly pointed us to stick with inflationary assets and value.

As long as this one mantra holds out:

IN LIEU OF ROATION, THERE WILL BE VOLATILITY.

Currently, we have rotation, so make hay while the sun shines!

So far, the growth-to-value rotation I spied is still holding firm.

Our client Trend Long Portfolio AND the Swing Portfolio (practically all longs) continue to delight.

So too do the Trend Fave & Swing Fave Watchlists!

In fact, for one hour Thursday morning I had ALL GREEN positions in my multi-week SWING PORTFOLIO of 20 positions for clients, which is a feat I tell you!

(Also ALL GREEN in client's multi-month TREND LONG ONLY portfolio, but that's expected since I am fiercely selective in this set-it-and-forget-it playlist.)

Here is a review I did for clients last Thursday before the holiday weekend to highlight how these plays look good - even though I see fewer and fewer NEW plays setting up (besides metals & miners): March 28th Portfolio & Fave Watchlist Review

Also last week, our resident doctor & BioPharma Analyst, Dr Alex Kenton, prepared a slide deck and key points to consider in assessing the players within the GLP-1 space.

Then we got together Wednesday and did a webinar! Thank you Alex for these insights on how to value the space!

The Big Bang in Weight Loss Pharmaceuticals w/ Dr. Alex Kenton

Again, Welcome Back!

And I wish you all a great trading week!!