Lions and Tigers and Bears, Oh My

After setting records in 2023, bulls came into the New Year afraid of something! Was it the bouncing US 10Y or dollar? Fed rate cuts getting priced out or fear of deflation priced in?

Either way, we set out on Tuesday with the worst start to a trading year for the Nasdaq Composite in its history after SPY ended 2023 within 1% of a record closing high and a 9-week winning streak. Only reason the Dow managed gains was thanks to healthcare stocks and the rotation into safety and staples, utilities and energy.

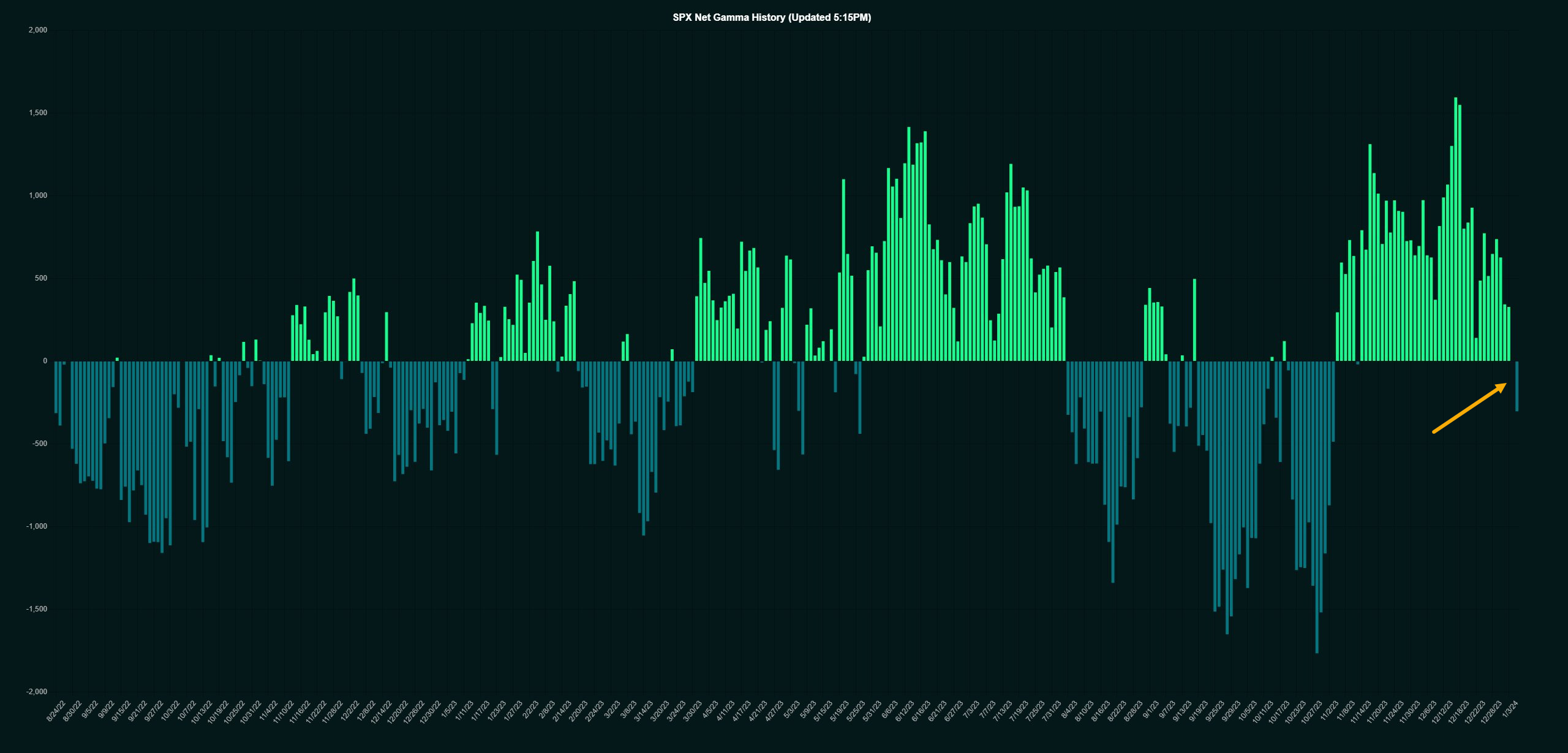

Wednesday continued the theme. We hit an important 'flow' threshold: Dealer gamma flipped negative below $4,750.

Chart h/t @GammaLab_tweets

But we need more selling to really trigger CTAs.

Nomura's from McElligott weighed in on Dealer positioning:

"The “perpetual hedging budget” of the VIX Call Buyer is still burning prem and lugging a ton of Feb VIX Upside which has Dealers Short, and still then risking “accelerant flows” on any Vol squeeze catalyst".

Translation: Dealers are still pressing their bets and shorting VIX.

If it's just for a trade: $VIX > 14.49 will ignite a scramble for calls.

But really, market is tight/neutral between 4750 and 4650.

For swing traders, that means: bullish above 4764; very bearish below 4600.

But most of the recent 2024 predictions don't expect a sell-off anytime soon.

Goldman sees S&P 500 EPS growth of 5% in 2024, with the index climbing to $5,100 by year-end.

BofA is even more aggressive, saying a $5,400 target level is probable, if not conservative in what it sees as year-two of a bull cycle.

Additionally, BofA’s sell-side indicator signals the most bullish sentiment in over 18 months after the largest month/month gain in over three years and second consecutive month of improvement.

I contend that hedge funds would need to cover more of their shorts AND add to new longs in small-caps before a resumption higher is in the cards. Breadth matters to market returns.

Unless this follows a 1999 Playbook, which I discussed with CLUB/EDGE clients this morning in my live trading room.

FOMC Minutes Released Today

We had a few economic data releases today: JOLTS wasn't very jolting, but ISM manufacturing showed continued contraction - timing perfectly with my call for a chase TLT bounce this morning in my live trading room (see chart).

We had continued yield softness after the FOMC minutes were released.

Here is a great summation from our very own Craig Shapiro, LaDucTrading's MacroAdvisor EDGE Manager:

“The Fed seems to be elevating the importance of "financial conditions" again, discussing the easing in the first paragraph of the minutes, much like they did in September when they added "financial" to the statement regarding tightening conditions. They should have taken the word "financial" out of this meeting's statement but didn't, however, this mention in the first paragraph of the minutes elevates the importance of it again. This suggests that significant loosening of financial conditions is self-defeating and will cause them to be on pause for longer, pushing back against the market expectations of imminent cuts and of 5-6 cuts this year.

The easing in financial conditions reversed some of the tightening that occurred over the summer and much of the fall.""Furthermore, participants observed that, after a sharp tightening since the summer, financial conditions had eased over the intermeeting period. Many participants remarked that an easing in financial conditions beyond what is appropriate could make it more difficult for the Committee to reach its inflation goal.

They also didn't speak about rate cuts at all in the minutes. If they wanted to emphasize that rate cuts were imminent, they would have done so. Instead, it seems they only really discussed cuts as they pertained to the DOT plot, which is what various Fed members had said after the meeting took place.

To me, this seems like a Fed attempt to push back against the market's rate cutting expectations. It may not ultimately work as we will have to see the rest of the data this week and in coming weeks but to the extent the data holds in ok (4Q Atlanta Fed GDP of 2.5%), there will not be a rate cut in March unless financial conditions were to tighten significantly again in a risk off event.”

An Alternative Macro Event Risk Position - Is Deflation now the risk if they don't cut?

Riddle Me This:

Fed was slow to hike "so" inflation took off higher.

Fed aggressively hiked - fastest in history - to play "catch up".

Inflation has decelerated back to neutral, but Fed has not cut.

Is Deflation now the risk if they don't cut? Hmmm.

Let's briefly go back and review my thesis in mid-Nov that Fed would cut. My macro-to-micro call was based on these reasons, as shared with clients:

I saw in my intermarket and technical read early Nov that the 10Y would make a 'fake breakout, fast failure" at 4.9% and reverse hard, falling fall back to 4%. I needed a narrative to go with my chart read, for at the time, no one was discussing cuts - not even me.

"USD Has Likely Peaked" was my macro-to-micro position in both long post form and interview Nov 9th.

I couldn't help but wonder should the 10Y stay at/above 5%, the wave of corps refinancing in 2025 would turn into a wave of defaults. I believed that Fed was going to cut to make it more manageable for banks to recover with CRE needing more time to repair/reposition, and of course, for struggling (read: unprofitable) companies not to die under the weight of spiking funding costs.

So far, that thinking or timing didn't suck. The 10Y fell precipitously into 3.8% yearly support - my overshoot target and "line-in-sand". And now all you hear about is whether or not the Fed will actually follow through.

Here's my thinking on the subject...

January 11th we get December's inflation data (CPI). I doubt it's strong.

So with that, I give Fed a >40% chance that they announce at their Feb 1st FOMC meeting they will cut for their March 22nd meeting.

I know. I know. This is NOT consensus, but I was right about the call I made in Nov that they would announce their Pause AND pull forward SEP (potential cuts) in 2024.

I think I have a decent chance to say they will follow through.

What I am unsure about is whether Yellen will issue more bonds than T-bills at the Jan 31st QRA (quarterly refunding announcement). If she does, this is market bearish, as it would spike both dollar and yields. I get a sense she may not - this round.

As a reminder, August 1st she issued more 'bonds than bills' and market liquidity was sucked out, so equities fell into the Nov 1st announcement, where she issued more T-bills than longer-duration bonds, equating to ~$75B in added liquidity (according to Michael Howell of @CrossBorderCapital).

My read of the charts says any near-duration (next 1-3 months) strength in dollar and yields will be range-bound and/or repressed.

There is always the risk from BOJ meeting Jan 22/23... that they surprise with an announcement of normalization, but the BOJ has not raised rates since 2007. I don't think they do it just before earnings season. And I don't think they do it before Fed announces they are cutting rates.

There is also the mechanism we have seen repeatedly around these congregated macro meetings - like FOMC, QRA, BOJ, ECB - wherein large USD swaps enter so as to manage these macro event risks.

Given all of the above, and being that I'm a betting woman, I would say that:

US 10Y yields MOVE violently intraday next few weeks into 4.1/4.2% before getting rejected, and reversing lower.

DXY bounces off $100 into $104/105 before getting rejected, and reversing lower.

USDJPY moves into 145/146 before getting rejected, and reversing lower.

Wouldn't it be ironic if this happens AND times with CPI (soft, pulling forward cut expectations), BOJ (pushing out normalization), and/or FOMC (pulling the trigger on announcing cuts)!

The bigger unknown to me will be whether we see a repeat of the Nov 1st "Yellen Yahtzee" I have written about. I'm sure that within the next month I will have more to say in preparation for the fateful Feb 1st event. For now, I just wish it didn't time with earnings season, for often times, we have the biggest market moves before earnings kick off, then chop sideways while we eagerly await MAG7 reports. Best bet: she threads the needle until April. April should be volatile.

Parabolas Reversing Oh My

In prior posts I have updated my 5 Core Swing Long Watchlists that did exceptionally well off the November/December rally for with CLUB/EDGE clients. Well, Dec 20th I started a new watchlist for clients - that we review in my live trading room, and this one was for set ups short.

It is entitled PARABOLAS for the obvious reason. And these are not the baby-bio or meme stocks you often associate with parabolas. They are simply a list of the clearest examples of overbought stocks/etfs I saw that looked ready to roll over.

All 15 are green for a cumulative gain of 75%. Not a bad start for the new year.

Trading Room Notes Summary

My main warning this morning to CLUB/EDGE clients before I closed my trading room at 11am ET was this:

SPX 4707 IS SUPPORT UNTIL IT ISN'T

QQQ at 400 PT, but I still expect expect to see 394 with SPY 465, SPX 4655.

VIX cheat sheet: below 13.85 market bounce, above 14.49 market trounce.

SMH gap down on wkly to 165.44 PT hit so likely bounce before further pressure, but big picture we need to break back below 163 to really make bulls sweat.

NYSE breadth has not rolled over and net selling has just started to break below 8D. That's the 1st big character change in the market we need to see for VIX to erupt.

As I like to say: "In lieu of sector rotation there will be volatility."

Actionable Trades

The best Chase short was a set up rejection of TSLA at wkly rejection of 263.55 back to daily gap fill of 240.30. We hit today.

The best Swing longs continued to be in Consumer Products/Staples: I mean food names (CAG, CPB, GIS, HSY, K, KHC, SJM) are doing some heavy lifting.

Congrats VZ + T swing long holders since last earnings (not me as I wasn't patient but glad you were).

ADBE was a nice continuation short from pre Xmas

TAN plays rolled over on this recent 10Y bounce. I removed ENPH from swing long just last week after a 49% advance on the underlying.

Trend long plays - STNG (+82.7%) and MCK (+114%) - made new monthly highs.

See you in the trading room tomorrow!