Crash Puts

This week, the equity market finally caught on (and down) to the carnage in the high yield bond market where both rate and credit spread exposure have combined for a growing toxic mix.

As such, we took out those May lows as I predicted, but did not spike higher in VIX as expected. (Still, the bull risk reversal in VIX as entered in #global-sector-rotations is doing just fine, thank you very much, along with swing short index and megacap tech puts.)

To date, SPY has dropped 23.5% below its all-time closing high - larger than the 1987 crash but occurring over half a year,

The fall in the Nasdaq is even steeper than the Covid crash in 2020 - down 33.7% - but I contend is still not oversold.

In the last six sessions alone, SPY has lost 10.9%. On Thursday, the index reached its lowest close since December 21, 2020.

That means, those who bought at the top need the index to gain more than 50% to break even.

How dare I propose that we have more to fall given this slow-motion train wreck?

Because I see the train on that proverbial bridge that collapses like in those old-time movie scenes. Slowly then all at once.

Crash puts are still my baseline bet as best hedge for lower prices in markets.

BOJ Punts

So BOJ announced they will buy more of their bonds and hell with the yen.

Loosely translated that means they rather US rates rise then have their government pay higher rates since they have like 270% debt/GDP.

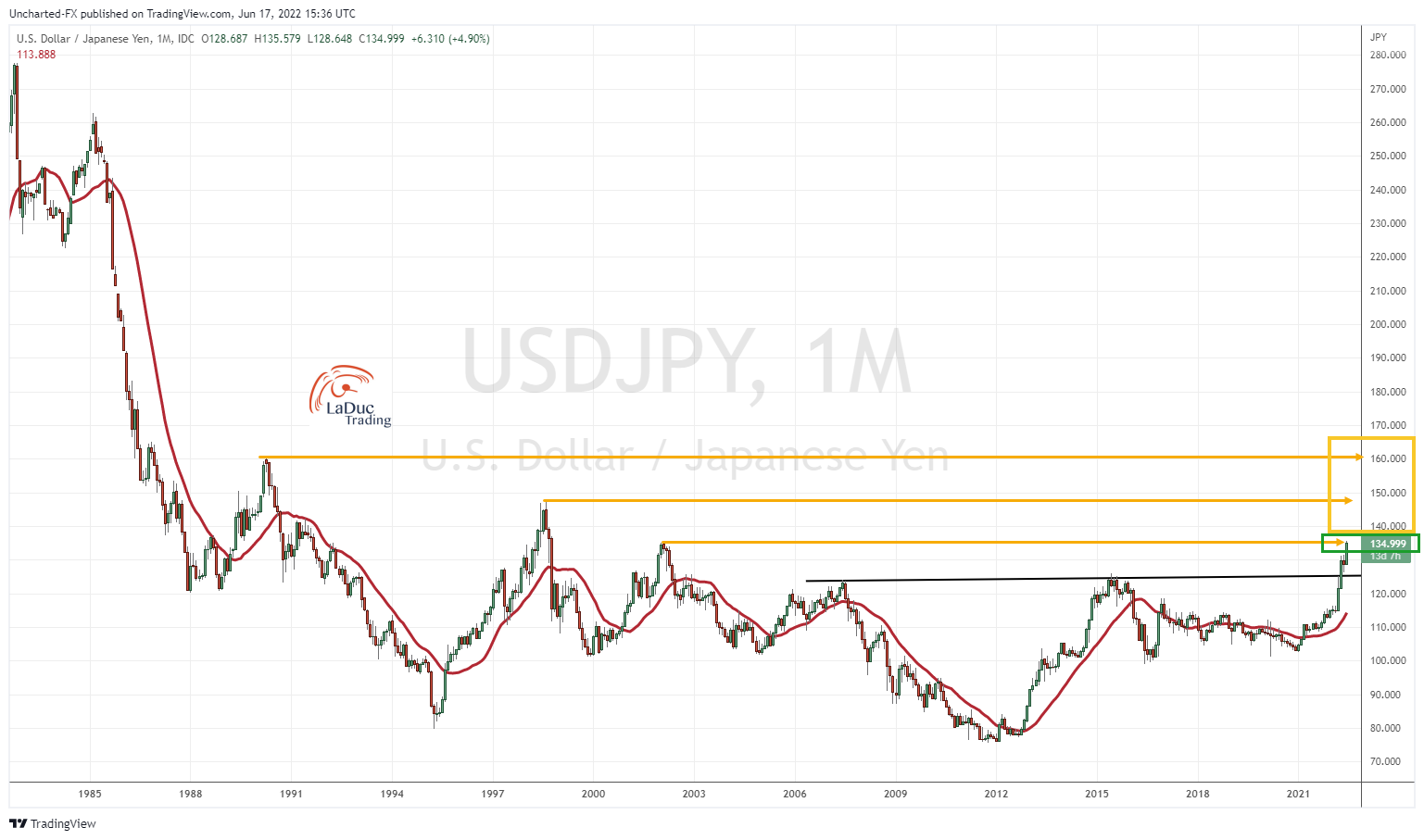

But just how long can the Bank of Japan stay super-easy when the world is going the other way? It is this very tension that’s pummeled the yen to 24-year low versus the dollar (before and after the meeting) and I contend is going lower (or higher if you are long USDJPY).

For macro risks, this is about as big as the come. With Japan dependent on importing commodities (especially oil and gas), a falling yen only imports more inflation which will only drive their CPI higher which will only make it harder for BOJ to keep their yields pegged near zero. BTW: May CPI in Japan is released next week and expected to be 2.5%. What if it surprises upward materially?

In a nutshell: The lower the yen, the higher their inflation. The higher the inflation they import, the more likely they trigger a fault line in their YCC, and once the fissures start, tremors will be felt around the globe.

Japan is the last general in the fight. All other major Central Banks have fallen to rate hikes and QT. When the experiment that is the BOJ fails, the war against inflation will be lost. The Inflation Monster (Godzilla-like) will cause a tsunami that emerges from the earthquake of failed CB intervention that crashes against all shores.

So this is a super-hyperbolic way for me to say that I fully expect the yen to fall fast + furiously while market implodes + yields explode.

Crash puts are still my baseline bet as best hedge for lower prices in markets.

Fed's Mudslide

Not to put the BOJ before the Fed, as Fed came first this week in their surprise announcement, but BOJ is clear in what they are doing; Fed really isn't.

They admitted to run-away prices and committed to 75 basis point hike and likely next meeting in July. This was the largest increase since 1994 so it's a big deal. But there other messages are mixed:

They still see inflation as a 2022 problem that fixes itself in 2023, but they've never had one call right on inflation, so why believe them now?

As for GDP growth, estimates for this year and next are sharply lower, but Fed says GDP will grow, and not decline, in both 2022 and 2023 - again, defending their 'soft landing' rhetoric.

Again, why should we believe them?

At least Powell fully admitted the Fed can't control Energy prices, so the White House sent out some press releases for oil intervention and helped them fall from overbought just in time for the thin opex liquidity ahead of a long weekend! Another thing they know how to do: suppress volatility and manipulate gold.

So it would 'appear' my main macro themes are being challenged of HIGHER dollar, yields, oil + gas. To which I say: Give it time.

I am still betting that the USDJPY moves higher: trigger is $135 (see chart) with $142 minimum/$147 overshoot, before the BOJ peg (yield curve control) breaks, setting free the yen to move higher and bonds lower. So think of it as the INFLATION before DEFLATION.

In the meantime, SO many price targets have come into play on Swing Short timeframes JUST as it looks like the market could careen over a cliff, making it more compelling for me to wait until next week to fashion my next directional bet. For now, I'm holding all the bearish growl especially given none of my #intermarket-tells have indicated a safe swing long let alone capitulation selling. For me, as I've warned, the market is still not safe, and at a growing risk of a Flash Crash into an Air Pocket of Risk.

Staying long the VIX hedge, adding Gold long next week, and staying long the Oil + Gas patch, with protection as warned last week (6/8) until I can see 'the turn' back up, all the while staying short indices and tech. No cheeky gap up trades for Tuesday post OpEx. I'm fine if I miss a big spike up because...

Crash puts are still my baseline bet as best hedge for lower prices in markets.

Reminder:

Markets and my trading room are closed Monday. Enjoy the day off and rest up as I bet it will be a bumpy week!!