Boring Doesn't Mean Bearish, Yet.

Chop is just another way of expressing range-bound price action until market decides which way it really wants to go.

Don't get me wrong: market is overbought! But that doesn't mean bearish. It means we need a trigger.

In the short-term, we have CPI Thursday morning consensus (0.2-0.3% expected), which has been market-moving in the past when it has come in soft.

The Nov report for Oct saw markets gap and go (11/14). Again, the Dec report for Nov saw markets move strongly higher (12.12).

Will this Jan report for Dec repeat to push USD and 10Y lower so equities can rally?

Currently, USD is firm; a break higher above 102.82 will put some pressure on equities. A soft CPI should soften the dollar.

But, bond traders are positioned for the 10Y to rally to 4.1% by Friday.

See Bloomberg article screenshot with the bet for the 10Y futures $111.50 put strike of size in the event of a treasury sell-off. H/T @parrmenidies

It could just be a hedge on event risk, but it coincides with SOFR longs getting cut three weeks in a row.

Where's The Meat of The Next Durable Market Move?

Yes, NVDA continued higher as a major beneficiary of the CES conference underway - past my $532 PT given yday morning. (Pelosi must be very pleased with here recently added long leaps.)

And AMZN above $146 is just bullish - and that's all I'm gonna say about that.

But pulling back from the big tech chases long and healthcare swings, there is no new theme yet for me.

I also see no net selling or breadth breakdown of size. We are correcting in time not price.

As I have reminded in my live trading room and here, I had a thesis coming into the new year that 2023 MAG7 winners would get sold. Then my growth-to-value indicator broke trend, so I expected a bounce in growth. We are right back up under that trendline! So now what?

Well, until we get back above that 1.86 ratio level, I don't see a solid reason for markets to run aggressively higher.

I also reviewed and posted my #intermarket-tells for CLUB/EDGE clients yesterday:

We are very overbought by so many metrics. Much different from when Powell & Yellen punted November 1st triggering a short-covering rally for the history books.

Trouble with being at an inflection point for growth and value stocks... we could chop violently intraday until Feb 1st when FOMC and Yellen's QRA bond issuance is revealed, settin the stage for the next durable directional market move. Either we lift off - 1999-esque - or pullback to minimum $4600 with overshoot to $4300.

Bitcoin ETF announcement is the obsession (not mine), and * may * come as soon as tomorrow, but chances of that happening are waning.

We had a taste of the price outcome today when the @SEC X account was apparently hacked, which resulted in GaryGensler making a statement denouncing the fake news of Bitcoin ETF approval.

Begs the question: if it WAS already approved, why would he have to announce that SEC has not approved the listing?

Bitcoin after-hours spiked higher to $48K before reversing back down to $45K area.

In the last few days, MSTR (often used as a bitcoin proxy) has sold off aggressively, now down 16%.

I still see this as Buy the rumor, Sell the news.

Also, Banks report Friday pre-market: Buy the run-up, Sell the event?

USDJPY is below 145 (which consists of 5 levels of daily resistance, so above is very bullish)... so if that changes, we will have potential for USD + US 10Y spike. Otherwise, we won't.

Japan has 10Y bond auction tonight. Keep that level in mind. It's important.

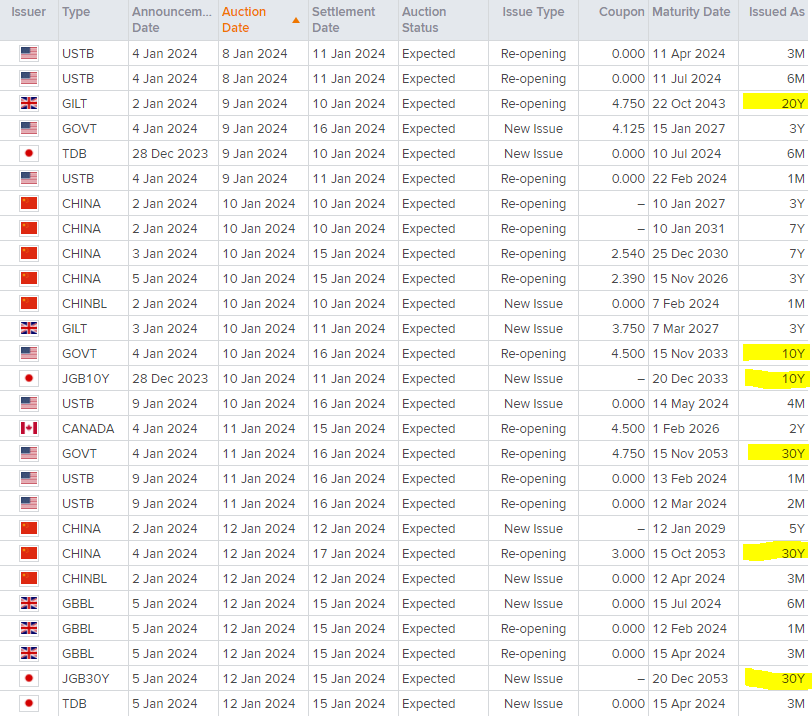

Chart h/t @Scutty listing the activity this week with 10Y bond auctions across US, UK, China and Japan

In the meantime, gold/silver/miners look weak.

Energy short looks strong (XLE).

And Coal is not moving higher until dollar pulls back - so better entry in 2+ wks.

Again, despite opening up with a gap down, SPX + NDX soon reversed and moved higher - led by Amazon and Nvidia.

But otherwise, I see no edge, yet, given the market is "Overbought But Not Breaking".

It's boring but that doesn't mean it's bearish...

Earnings Reminder

We’re hitting Q4 earnings season with low expectations (see chart). Goldman is looking for S&P 500 firms to beat analyst forecasts in aggregate in Q423, despite a higher bar relative to recent quarters.

For Q3, the S&P 500 had earnings growth of 4.9%, and analysts expect growth to slow down to 2.4% for Q4.

Analysts expect quarterly revenue growth of 3.1%.

For the year, the S&P 500 is expected to post earnings growth of just 0.6% and revenue growth of 2.3%.

My bet: We already priced in rate cuts and Wall Street analysts have cut their Q4 2023 earnings estimates far more than is usually the case. Earnings will beat more easily, but have to really delight to trigger a strong market reaction higher. Given earnings are by nature a reflection of how things have been rather than how they will be, guidance will be more highly valued.

There is one sector I will be tracking closely to chase post earnings, and for options flow pre-earnings: Retail.

Consumer was spending by many accounts - especially on credit!

US consumer credit rose sharply in November, exceeding $5 trillion for the first time. See chart.

Not to mention:

Debt outstanding rose nearly $24 billion in November, Fed says Households’ credit-card balances rose most since March 2022

Bloomberg

In a nutshell, there are a bunch of oversold retail plays (left for dead) that could look like good #chase-ideas or even #swing-ideas, especially since the broadline retail industry is expected to report earnings of $30 billion this year - up from a loss of -$1.2 billion last year.

Quant & Positioning

There's concentration risk and then there is extreme levels of concentration risk:

We already know that US equity index futures net longs are extended. I've written about CTA positioning in recent posts.

But... Nomora's McElligott explains why the long positioning continues given skew is depressed:

"Index level Call Skew remains historically “bid” as folks have undercaptured the Equities rally, which means we still aren’t seeing enough underlying Net Exposure to necessitate big big Hedge buying that puts Dealers into a “Short Gamma / Short Vega” pain position in the case of a Spot selloff—hence, Skew, despite a modest recent uptick, just remains too lukewarm for any potential “outlier drawdown” fireworks at this juncture".

Overall, positioning is stretched like the market, but not yet bearish: H/t @TheMarketEar

1. GS prime book LS at 86th percentile over 12 months.

2. CTAs with long positions at 95th percentile over 12 months.

3. Put-call skew at 8/10.

4. GS Risk Appetite indicators for monetary, growth components, and positioning sentiment in stretched territory.

It's not a stretch to say the Santa rally ended in 2023, active fundS are with stretched long positions, and chances are growing we will mean-revert.

We just need a trigger.

This is great stuff!